Public sector accounting in Europe

Feb 2, 2016

A post by Nicolas Kayser-Bril of Journalism++

In the list of the things you care about, the different types of public sector accounting standards probably rank right between Kim Kardashian’s latest haircut and the state of research on the spirituality of snowboarding. That’s normal, but it’s more interesting than you thought.

The way public officials record how they spend the money you give them is of tremendous importance. They can make it look like they’re doing a terrific job when they’re driving the city finances in the ground. They can make it look like they’re debt-free when they, in fact, signed contracts that bind your children, your grand-children and their grand-children. And they can make it all up as well - that’s how scrutinized this aspect of public government is.

Historically, accounting was done very simply. Make a table with a column “money in”, “money out” and “balance”. When you collect money, write it in “money in”. When you spend, write it in “money out”. Either way, update the “balance” column. That’s what your own banking statement looks like and it’s a great way for anyone to keep track of spending.

Let’s take a fictional example using cash-based accounting:

| Date | Balance | Money in | Money out | Name of transaction |

|---|---|---|---|---|

| 2 Jan | 1,500€ | 1,500€ | Loan from the bank | |

| 3 Jan | 1,050€ | 450€ | Subsidy to mayor’s football club | |

| 4 Jan | 800€ | 250€ | Reception at city hall |

It’s older than gun powder

What’s a great way for us to keep track of spending may not be so smart for larger organizations. If you follow this cash-based accounting and take a loan, your cash reserves will increase a lot. Hooray! But maybe the loan you took is so huge that you’ll have a hard time repaying it. With cash-based accounting, if you make promises to someone (let’s say you offer to give away 3,000€ five years from now), it doesn’t show until the disbursement is made. That’s not great if you want to plan ahead. With cash-based accounting, if you make a mistake like adding a “0” too many to your income, you only realize your mistake when you check your accounting with your bank’s. And it might be too late.

Because cash-based accounting is so limited, humans developed a more robust accounting framework. In the 13th century. You read correctly. We realized we needed a good accounting system before we knew the Sun didn’t rotate around the Earth (200 years later) and before we knew we needed to wash our hands after we go to the toilet (500 years later) and before we realized it might not be such a good idea to feed booze to kids for lunch (700 years later).

This new version of accounting is called double-entry accounting. It’s mandatory for companies, but not for all public bodies.

Double-entry means that each time something happens, it is written down twice: once in the account where the money was received and once in the account where it was taken. For each credit operation, there is an equivalent debit operation. Bear in mind that “credit” doesn’t mean “cash on your account”. The meaning of debit and credit depend on which account you’re operating.

Each aspect of the organization’s activity has its own account. Not all organizations have the same number of accounts. It depends on what an organization does. A city in Finland’s far north will need an account for winter clothing for city officials, an account for snowmobiles, an account for de-icing salt and so on. A city of the same size in southern Italy won’t have such accounts (but they might have some for boats and nautical gear).

Let’s look at our fictional example again, done with double-entry accounting:

Loans Payable account

| Date | Debit | Credit | Name of transaction |

|---|---|---|---|

| 2 Jan | 1,500€ | Loan from the bank |

Cash account

| Date | Debit | Credit | Name of transaction |

|---|---|---|---|

| 2 Jan | 1,500€ | Loan from the bank | |

| 3 Jan | 450€ | Subsidy to mayor’s football club | |

| 4 Jan | 250€ | Reception at city hall |

Subsidies account

| Date | Debit | Credit | Name of transaction |

|---|---|---|---|

| 3 Jan | 450€ | Subsidy to mayor’s football club |

Reception account

| Date | Debit | Credit | Name of transaction |

|---|---|---|---|

| 4 Jan | 250€ | Reception at city hall |

It’s a slightly more complex than cash-based accounting but it lets you see immediately how much was spent on what account. Philipp Häfner, director at the court of auditors of Hamburg, Germany, compares double-entry accounting to a city’s operating system, like Android. Without double-entry accounting, it’s impossible to run apps like controlling, consolidation of accounts etc. he says.

The Appstore

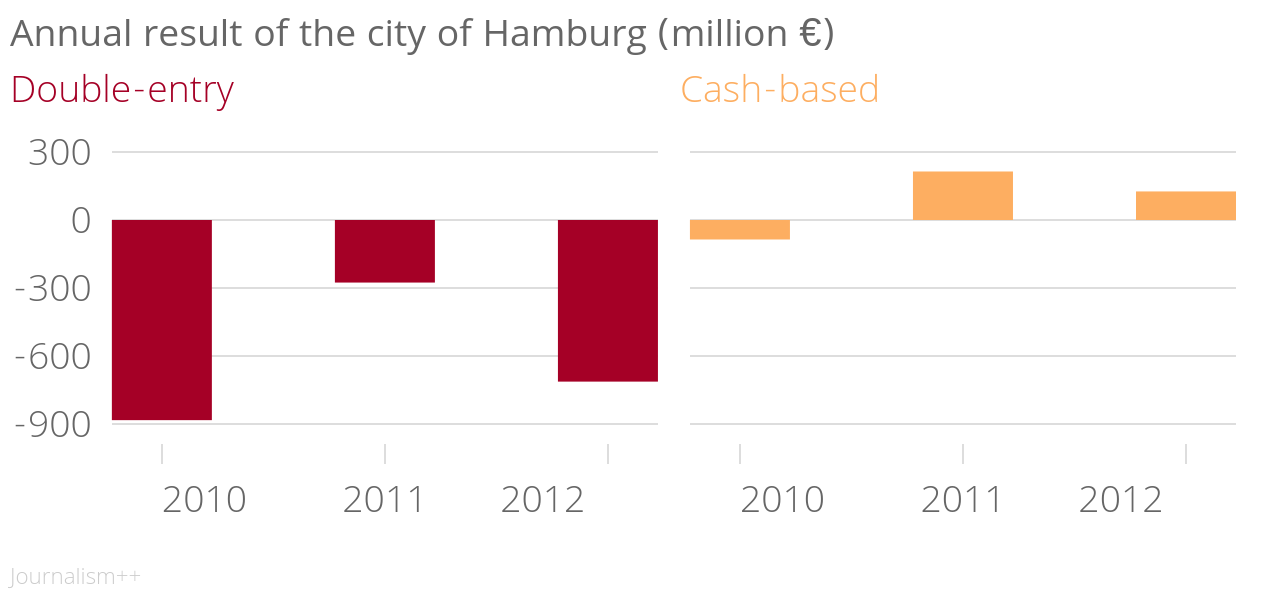

There are even more apps that can run on double-entry accounting. Mr Häfner compared the net result (how much money the city made in a year) of the city of Hamburg for 2010, 2011 and 2012. Here’s what he found:

The difference can be close to one billion euros. That’s about €600 per person who lives there! Why is the difference so huge? With double-entry accounting, you have accounts for the liabilities (the debt) you take. For a city, it’s important to keep track of the pensions it will have to pay in the future. If hiring someone now means that the city will have to pay a pension, the amount of that pension needs to be taken into account now as well. Same thing for buildings. With cash-based accounting, selling a building means a lot of cash in. With double-entry, you decrease the value of the account where the building was registered just as you increase the amount in the cash account. (As Jens Heiling, a technical manager with EY, an audit firm, points out, it’s possible to do it in a cash-based system as well. It’s just much harder, and the chance of error is much higher.)

You don’t have to get all the subtleties of double-entry accounting to understand that it’s way easier to hide your debt in a cash-based system.

Another reason why double-entry accounting is needed lies in the web of subsidiaries cities operate. For waste disposal, hospitals etc. cities have set-up semi-private companies. Hamburg has 300 such companies that ended up forming “conglomerates”, says Mr Häfner. These companies follow the double-entry accounting norms of the private sector. To consolidate accounts (to have a global view of the situation), accounting systems need to be compatible. Consolidating a double-entry account with a cash-based one is like trying to run the latest version of Microsoft Word on MS-DOS.

Comparing an accrual with a cash-based budget is nothing like comparing apples to oranges. It’s more like comparing fresh apples to french fries.

Why you should care

You might be thinking that this is all very interesting… for accountants and, maybe, nerds. You’d be wrong. Accounting has some very direct effects on your life.

In Europe, every country follows different rules. In Germany, where most public bodies still do cash-based accounting (Hamburg is one of the exceptions), no guidelines were written for organizations who wanted to move forward. As a result, anyone did as they pleased. Mr Heiling studied the university of Heidelberg and came to the conclusion that it designed its financial reporting system “according to its own preferences”. Its own preferences probably don’t include ‘making sure that the public has an easy access to our budget data’.

Because accounting in the public sector is such a mess, it’s often impossible to know precisely what a city owes to whom. Politicians can take huge commitments without having to write them down in the books.

Cities can take hazardous credits and not provision for the associated risk. In 2011, the city of Linz, Austria, lost over 30 million euros (160€ per person) because of risky credits it had taken. Ironically enough, its head accountant published a series of rants against double-entry accounting in 2008. For him, double-entry accounting was a neoliberal trick to let private auditors like EY sell more stuff to cities. The dramatic incident in Linz was not due to its accounting system (cities practising double-entry accounting also suffered), but double-entry accounting could have helped see the risk before it became real.

Germany is famous for its derelict infrastructure. In cash-based accounting, a new piece of infrastructure is a one-time expense. In double-entry accounting, assets have their own accounts. As they age, their value decreases (it’s called “depreciation”). It shows what needs to be re-invested to keep an asset up-to-date. While it’s an overstretch to say that double-entry bookkeeping would in itself improve infrastructure, it makes the issue of timely reinvestment harder to avoid, Mr Häfner said. In Hamburg, double-entry bookkeeping helped the city better plan its infrastructure spending.

Accounting is way too important to be left to accountants alone. And in the end, citizens - not public officials - pay for past mistakes.

Sources

Yes, until 1956, parents could and did give wine to their kids for lunch. In France at least.

An interesting presentation from 2007 detailing the state of double-entry accounting in Europe.

Here’s a well-writen tutorial on double-entry accounting, if you’re into this.

The paper by Jens Heiling on the university of Heidelberg.

That’s the 2008 anti-double-entry rant by Linz’ head accountant. If you read German, you’ll enjoy the lyrical style. Here’s a story from 2011 about the financial catastrophe in Linz and Vienna.

Here’s a good ZEIT piece on the state of infrastructure in Germany.

And, because we need to keep in mind that it’s not all about accounting, you might want to read on the spirituality of snowboarding and an analysis of Kim Kardashian’s haircut.